December 2025, a Series-C pitch in Singapore. Jenny Lee of GGV Capital asks the question that will define the next hour: "What prevents a well-funded competitor from replicating your architecture?"

The founder — call her Priya — answers without hesitating. "Any competent team could build comparable systems in eighteen months. What they can't replicate is three years of regulatory interactions codified into our compliance swarm, billions of transactions training our credit models, trust built through thousands of flawless audits." Jenny closes her notebook. The round is effectively done.

Eighteen months earlier, a different founder faced the same investor and the same question. He spent four minutes on his training-data advantage and his pilot metrics. Jenny's follow-up: "And six months after a well-capitalized competitor sees those metrics?" He had no answer. By the time Priya closes her Series C, he's still hunting for product-market fit, burning $800,000 a month. Same question. Opposite fates. The difference wasn't technology — they had the same foundation models. Priya had built something that got harder to compete with as time passed. He hadn't.

The conventional moat is the wrong map

For most of economic history, competitive advantage meant controlling something scarce you could point to. Land, in the agricultural world. Factories, machinery, patents, and distribution in the industrial age. The railroad barons who controlled routing through mountain passes held a moat that needed no fence — geography was the moat, and a banker could collateralize it.

This map still governs how most leaders assess defensibility. They look at the balance sheet: real estate, patent portfolio, headcount. And steel-manned, that instinct served well for two centuries, because in those eras the durable assets really were the visible ones.

The map breaks in the AI-Born economy. By 2020, intangible assets represented more than 90% of S&P 500 market value, while financial statements still showed factories and receivables. AI-Born moats live in the interaction between architecture and accumulated learning — how agents have been trained to behave, what edge cases the system has resolved, how deeply the platform has embedded into client workflows. None of it appears on a balance sheet. The assets accountants can't count are the ones competitors can't buy.

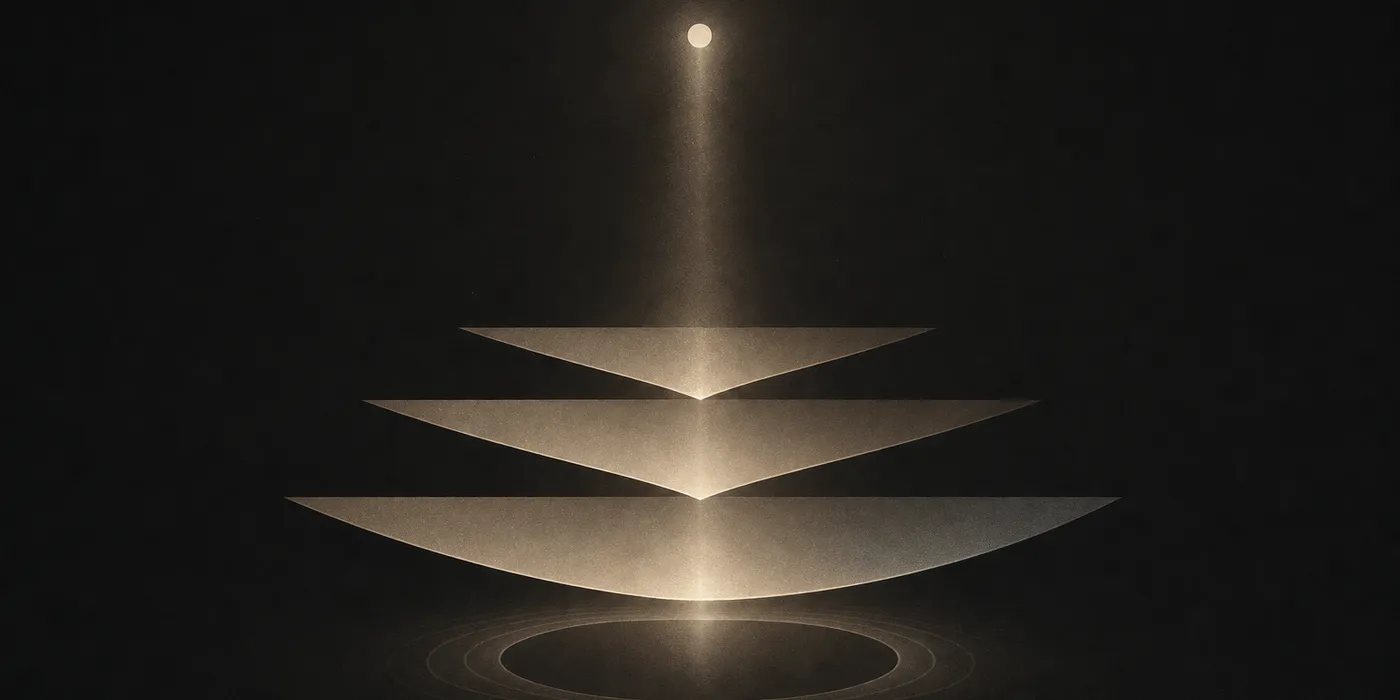

The reframe: five layers that compound, named A.G.E.N.T.

Three Singapore fintech engineers founded Meridian Trade Finance in 2022 — a composite case synthesizing documented patterns from AI-Born fintech across Southeast Asia. By year three, 47 employees processed more than $4 billion annually. Industry average ran roughly $7 million per employee; Meridian's architecture produced over $80 million — a 10× gap that meant a competitor needed 500 people to match what Meridian did with fewer than 50.

The difference lay in the A.G.E.N.T. Defensibility Stack:

- Architecture creates frictionless operations through elegant design.

- Governance transforms compliance from constraint into weapon.

- Evolution hardens systems through learning velocity.

- Network raises switching costs through embedding depth.

- Trust compounds from demonstrated values alignment.

Each layer strengthens the others. Architecture enables faster iteration. Evolution improves governance. Trust deepens embedding. Network effects generate data that sharpens architecture — and the cycle accelerates.

Figure: The A.G.E.N.T. Defensibility Stack — five layers that don't add up. They multiply.

The mechanism: how each layer feeds the next

Architecture sits beneath the stack, not atop it — scale amplifies whatever you built underneath. Meridian's [[coi-the-one-metric|Cognitive Overhead Index]] measured 24; competitors scored 71. Onboarding 50 clients a year took Meridian 2 people and competitors 14. Its customer acquisition cost dropped 40% annually as volume scaled while competitors' stayed flat. The architecture itself is reproducible; the learning crystallized into thousands of decisions about error handling and recovery is not.

Governance turns regulation into a weapon. When an audit flagged documentation problems in 2023, Priya halted all feature development for six weeks to rebuild compliance architecture — risking mutiny — and the investment paid back within nine months. The Monetary Authority of Singapore issued a commendation rare for a year-old fintech; Thai regulators compressed sandbox approval from six months to three weeks. Regulatory goodwill accumulated early is the one asset a competitor can't acquire by writing a larger check.

Evolution is iteration velocity, captured by [[iteration-half-life-compounding-clock|Iteration Half-Life]]. Meridian ran five-day cycles against StellarPay's 90-day quarters — roughly 70 iterations in year one versus four. Iteration #18 incorporates seventeen rounds of learning that StellarPay's iteration #1 can't match. Cursor rode exactly this dynamic from near-zero to more than $2 billion in ARR in roughly eighteen months, on the same LLMs available to every incumbent. You can't buy eighteen months of accumulated learning with a Series B.

Network converts customers into infrastructure dependencies. When Shopee reached Stage Four embedding with Meridian, replacement would have required rewriting trade-finance APIs across 14 internal systems at an estimated $40–60 million over 18–24 months. Shopee couldn't afford to switch even at 30% lower fees.

Trust determines who stays when competitors arrive. When StellarPay launched a 15% price undercut, only 3% of Meridian's clients switched — because the design philosophy embedded in 3,000+ architectural decisions couldn't be reverse-engineered from the APIs.

What to do

- Score your COI as a competitive forecast, not an ops metric. Above 60, you're not a slower Meridian; you're a different kind of machine that can't iterate fast enough to stay in the category.

- Build compliance architecture before you need it. Early regulatory goodwill compounds; late compliance is a fire drill.

- Measure your Iteration Half-Life now. Above 30 days and you're watching AI-Born firms from the other side of a gap that widens every week.

- Track Embedding Coefficient stage per major customer. A Stage One relationship is not a moat. Design integration depth deliberately.

- Map your trust-destruction scenarios before a failure forces you to. Survivors aren't the ones with perfect records — they're the ones whose transparency infrastructure reconstructs what happened in hours, not weeks.

The principle

This isn't a framework where 4 out of 5 is a passing grade. Olive AI raised $852 million with strong Architecture and Governance, but Trust never scaled beyond pilots — so Network never emerged, and there was no moat to defend when cash ran out. A wheel missing a spoke doesn't spin slower. It fails under load. Build all five, and late entrants face not just your current capabilities but your accumulated learning, embedded trust, and regulatory goodwill — none of which has an acquisition price.

Adapted from the essays accompanying AI‑Born by Mehran Granfar. Themes drawn from Volume I, "The Machine Core".